Enrol

Capability Benchmarks develops examination-based professional certifications for sustainability assurance practitioners. Every credential is built from regulatory obligations, tested under examination conditions, and designed for practitioners who must defend their work.

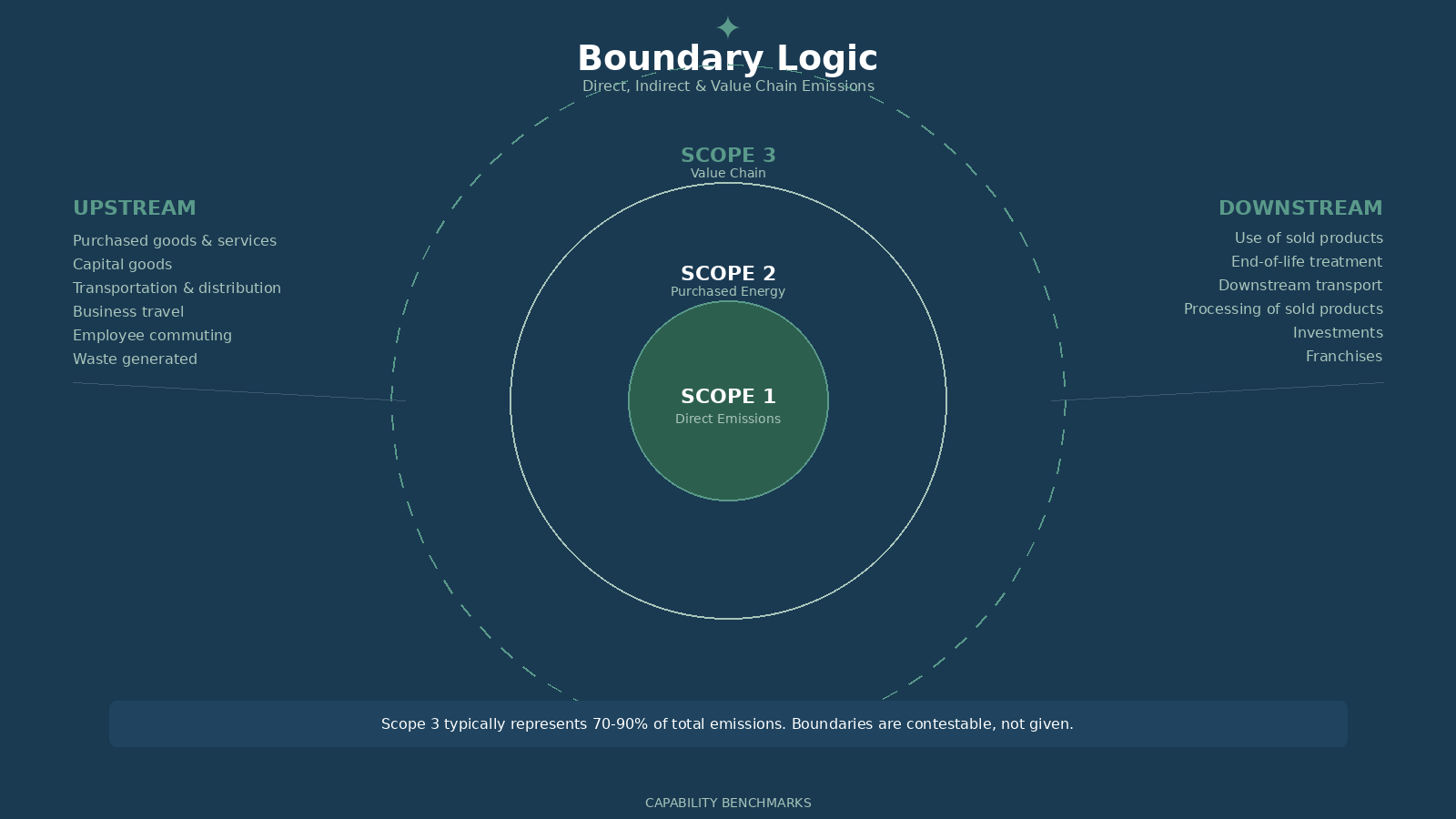

Scope 3 emissions present assurance challenges that go beyond conventional financial audit or operational review. Value chain data involves estimation, allocation, and methodological choice at every stage. Boundaries are contestable. Evidence hierarchies are unclear. Completeness cannot be verified through conventional means.

CS3-SCA addresses these challenges directly. The programme develops the reasoning capabilities required to form defensible conclusions under conditions of inherent uncertainty and to document that reasoning in ways that withstand regulatory inspection.

This is not introductory sustainability training. The programme assumes professional assurance experience and familiarity with GHG accounting concepts.

The CS3-SCA programme is comprised of eleven modules covering boundary logic, evidence hierarchy, materiality assessment, assurance conclusions, independence, regulatory defence, and integrated professional judgement. All modules are mandatory. Completion of the programme provides access to the certification assessment.

Certification is awarded only upon passing the assessment.

CS3-SCA is designed for professionals with existing assurance, audit, or verification experience who are working with or preparing to work with Scope 3 emissions disclosures. This includes:

The programme is not suitable for those without prior professional experience in assurance, audit, or verification disciplines.

Financial reporting has never required perfect measurement. For centuries, critical figures in audited financial statements have been based on professional judgement rather than precise calculation.

The fair value of an asset is an estimate. A provision for future liabilities is a judgement. An impairment assessment involves assumptions about conditions that have not yet materialised. These figures are not exact and they are not expected to be. What matters is that the methodology is permitted, the assumptions are transparent, the judgement is defensible, and the documentation supports the conclusion.

This is the same logic that governs Scope 3 emissions reporting.

Value chain emissions cannot be measured with the precision of a bank balance. They involve estimation, allocation, and methodological choice at every stage. But this does not make them unreliable or unauditable. It makes them subject to the same professional discipline that has governed financial reporting for generations: reasoned judgement, applied consistently, documented thoroughly, and defensible under scrutiny.

Scope 3 reporting is not experimental. It is the application of established professional standards to a new domain. The uncertainty is real. The framework for navigating it is not.

Examine the full syllabus, module structure, and assessment format before enrolling

Programme